Time flies in the market, but there’s one name that always seems to sit comfortably in big institutional portfolios MSCI. Honestly, most people just know them as the guys who make indices, but when you dig into their guts, this company is actually a high performance money printing machine. In this article, I want to break down why I’m keeping a close eye on this stock using some solid fundamental data plus a quick look at the technicals to see if it’s currently a steal or a skip.

Revenue That Never Looks Back

Check out their annual revenue growth chart from 2017 until now.

To me, this is the definition of a dream chart for long term investing because it moves up steadily like a staircase. From 2017, where revenue was around $1.27 billion, it’s now sitting pretty at $3.23 billion (LTM). That’s a total increase of 154.24% with a 12% CAGR. For a mature company, that kind of growth is super stable. It shows that their ESG data indices and analytics aren't just a trend they’re a must have for fund managers worldwide.

Profits Growing Faster Than Sales

One thing I really respect about MSCI’s management is their ability to make profit grow even faster than their sales.

You can really see the operating leverage magic here. While revenue grew by 12%, their Net Income actually grew with a 19.5% CAGR. The total jump in profit since 2017 is insane up 334.16%. This means every new dollar coming in doesn't require a lot of extra cost to manage, so the profit just flows straight to the bottom line.

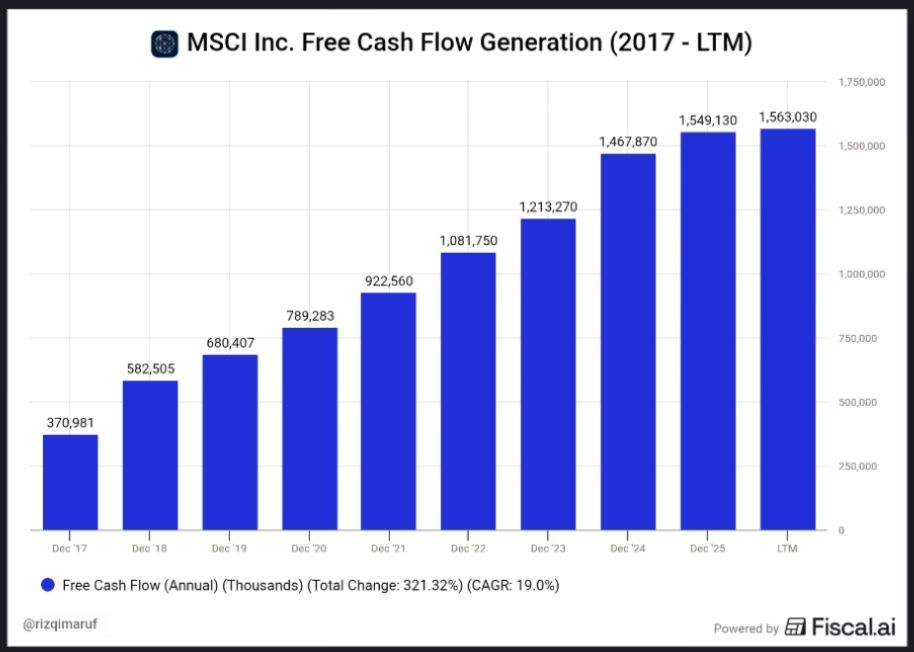

Magic Margins and Cash Flow

If we’re talking quality, we have to look at the Net Profit Margin.

Their margins are some of the thickest in the industry, currently sitting at 40.7%. It even peaked at 45.4% back in late 2023. It’s very rare to find a company that can maintain these kinds of margins consistently unless they have a massive moat that competitors can't touch.

Then there's the cash flow. MSCI isn’t just a company that looks good on paper; their actual cash is overflowing, with 19% CAGR growth. They use this cash to pay dividends or buy back shares, which eventually goes right back into our pockets as shareholders.

Finally a Price That Makes Sense

Now for the part every trader loves to argue about valuation.

Flashback to 2021, and MSCI’s valuation was honestly kind of nuts the Forward P/E soared above 60x. That was basically buying a dream. Luckily, the market has cooled off and given us a healthy correction. Now, their Forward P/E is at 28.75x. For a diamond tier company at a big discount from its peak, this is definitely something worth watching.

Technical Peek Chilling in Consolidation

I just checked the daily chart for MSCI, and it's currently moving in a pretty wide consolidation zone.

Price is currently holding around $581 after bouncing between $525 and $633. Looking at the indicators, the RSI is at 52.70, which is neutral. However, the Stochastic at 29.78 is getting close to that oversold territory. Usually, once it dips below 20, we might see a short term bounce. That $578 - $581 area is super crucial to hold.

The Future 2026 - 2028 Projections

I also took a look at what analysts are predicting for the next few years.

The future looks bright. Sales are projected to climb from $3.49B in 2026 to $4.10B by 2028. Earnings Per Share (EPS) is also expected to jump from 19.63 to 25.52. For the upcoming quarter (Q2 2026), EBITDA and EPS are expected to show solid growth of 6.70% and 6.50% respectively. If this plays out, the valuation will naturally get even cheaper over time if the price stays here.

Important MSCI News

To keep it real, I gathered a few key updates on what’s happening with MSCI.

Expanding in Asia According to Reuters, MSCI is doubling down on its dominance in the Asia Pacific region by launching new ESG indices focused on energy transition. This perfectly explains that revenue growth we saw earlier.

Solid Earnings Performance Based on the latest quarterly data from their investor relations, MSCI continues to report double digit revenue growth. Their subscription based model is proving to be incredibly resilient, even when the broader market gets a bit shaky.

If you check the latest sentiment on Yahoo Finance, analysts are constantly highlighting MSCI’s insane pricing power. Basically, because so many ETFs are tied to their indices, MSCI can raise fees without losing clients. This is exactly why those net profit margins are staying thick at over 40%.

Final Verdict Buy the Dip or Wait?

Honestly, MSCI is the kind of stock that lets you sleep at night. The fundamentals are rock solid, margins are massive, and the cash flow is undeniable. A 28x Forward P/E is way more friendly than what we’ve seen in years past.

Technically, we might have to be patient while it consolidates, but for long term investors, this area down to the support level is a sweet spot for scaling in. Remember, investing is a marathon, not a sprint so keep your money management tight.

What do you guys think? Is MSCI still the king of your portfolio? Let me know in the comments.

Keep trading and stay profitable:)

Source:

Reuters

Ir.msci

Yahoo Finance