Europe is moving ahead with its embracing of cryptocurrency. Unlike the United States which is trying to destroy this industry, Europe is taking the exact opposite approach. This is allowing financial institutions in that area to start innovating and bring out digital assets.

We now see the 7th largest bank in the area enter the stablecoin market. Societe Generale rolled out a token that is pegged to the euro.

Here is entry from a major [bank(@leoglossary/leoglossary-bank) into a market that was previously done by companies outside the traditional financial system. Outside of funding, none of the establishment entered the digital asset space to such a degree.

This is giving us insight into the direction things are likely heading.

Another Rival To Central Bank Digital Currencies

Among the cryptocurrency community, many feel that it is a given that central bank digital currencies (CBDC) will take over and drive all other forms of money out. This is misguided in that it is not keeping with monetary history. For the last 600 years, most money was private, mostly through the banking system. Governments had little direct control.

That said, this is another obstacle standing in the way. We can expect to see a flood of stablecoins brought out by banks all over the world. It will get to the point where most are offering it. As stated in the past, these will become like websites. If you are a business, and you don't have a token, you aren't in business.

End Of The Stablecoin Market As We Know It?

Another conclusion is whether this is a nail in the coffin for the present stablecoin market?

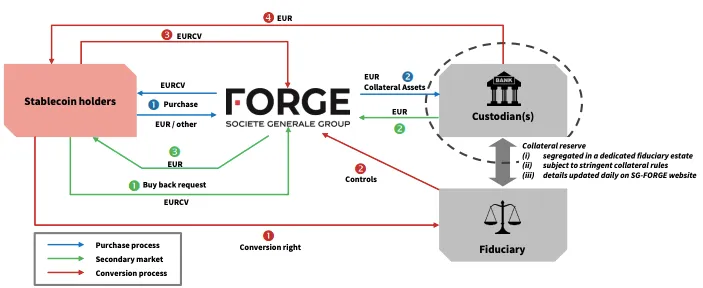

As we can see from the diagram, this is an asset-backed stablecoin. The bank will hold a combination of cash and securities. This is in keeping with what companies such as Circle are doing.

Some are right to question whether asset-backed stablecoins are really the future. Personally, I think it is going to be algorithmic stablecoins tied to other digital assets. The former approach is not really building a currency as much as basically establishing a money market account that is tokenized. They are actually two different instruments.

The other issue is we are seeing a permissioned system that is controlled by a bank. This enters counterparty risk into the equation, something present with all asset backed stablecoins. Societe Generale will act as the custodian for the assets, something it is accustomed to doing.

Of course, the stability of any bank, after recent events, should be questioned, especially in Europe. If we see this banking crisis growing, how strong are the entities that could be bringing out these coins.

The Impact Upon The United States

This action might actually kick the United States in the pants. While this is an asset tied to the euro, do not think for a second this is overlooked by the major U.S. banks. A JP Morgan and Goldman Sachs would love to get into this game.

Remember when the banks would claim they "love blockchain but hate Bitcoin". Obviously, that was a farce since we know they didn't like blockchain, at least not a decentralized version. Back then, "enterprise blockchain" was the rage with companies such as IBM touting that as the future. It went nowhere for obvious reasons.

Nevertheless, the bankers do like the idea of control. Circle will have to come under United States banking regulations regarding digital assets (once they are written). This is going to pit it against some of the larger institutions. Do not be surprised if a Circle is bought out by the likes of a Goldman Sachs.

It likely will only require a foreign bank to bring out a US dollar denominated stablecoin to wake everyone up. Imagine having to defend allowing foreign banks taking over control of the USD.

The odds of that happening are non-existent. For that reason, this is a warning shot.

The Impact Upon The Hive Backed Dollar

We discussed the Hive Backed Dollar (HBD) a great deal. Some might look at this as a threat to that currency.

For now, nothing could be further from the truth.

To start, Societe Generale token is based upon the euro. This makes sense considering the location of the operations. However, when looking global, the #2 currency is still regional for the most part. The reach of the euro is rather limited compared to the USD.

The evidence of this comes from areas such as Cuba, Venezuela, and Ghana. We keep harping on these areas because they are the epitome of the problem HBD is solving. Ironic, it is also the same problem those behind CBDCs are looking to address.

Who wants the Bolivar, Cuban Peso, or Cedi? Certainly not the people in those countries. If given a choice, most prefer to operate in dollars. Unfortunately, it is a banknote only situation.

HBD brings this to a digital level. Suddenly, there is a payment system in USD that have no transaction or merchant fees. There is instant settlement, occurring on average in under 2 seconds. This has great appeal to a couple billion people with smart phones but no access to the USD.

A second point is the permissioned part of Societe Generale's token. It is going to be based upon their requirements, focusing upon institutional clients. Thus, the average person is not going to be utilizing this. It will likely serve as the foundation for investment banking operations.

Then we have the control.

The smart contract code for EURCV was also panned on Twitter because Societe Generale will need to issue a transaction of its own to process every transfer of the new stablecoin.

Essentially, this is just another Wall Street type tactic. The stablecoin could be successful yet is limited in scope.

If you found this article informative, please give an upvote and rehive.